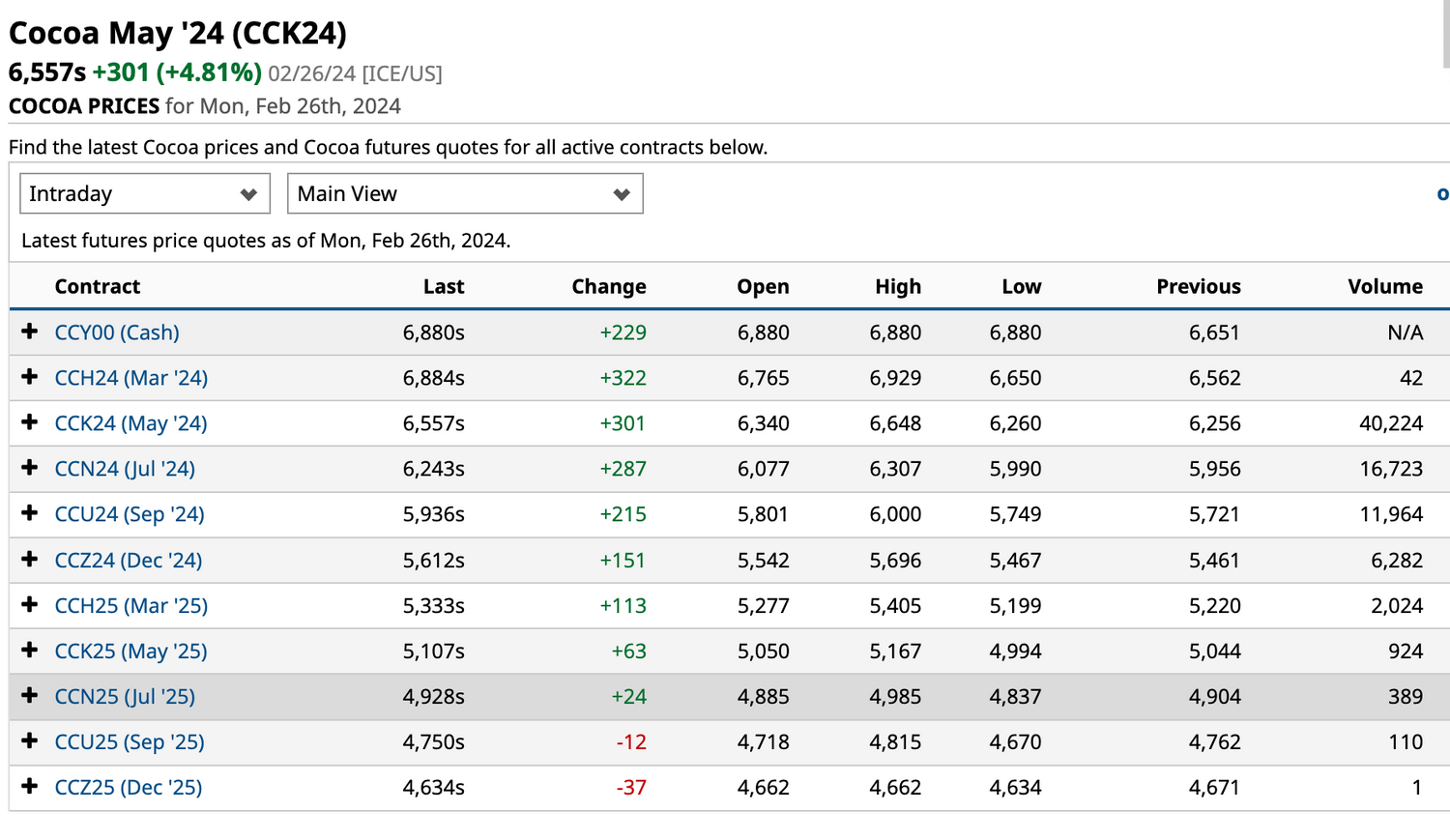

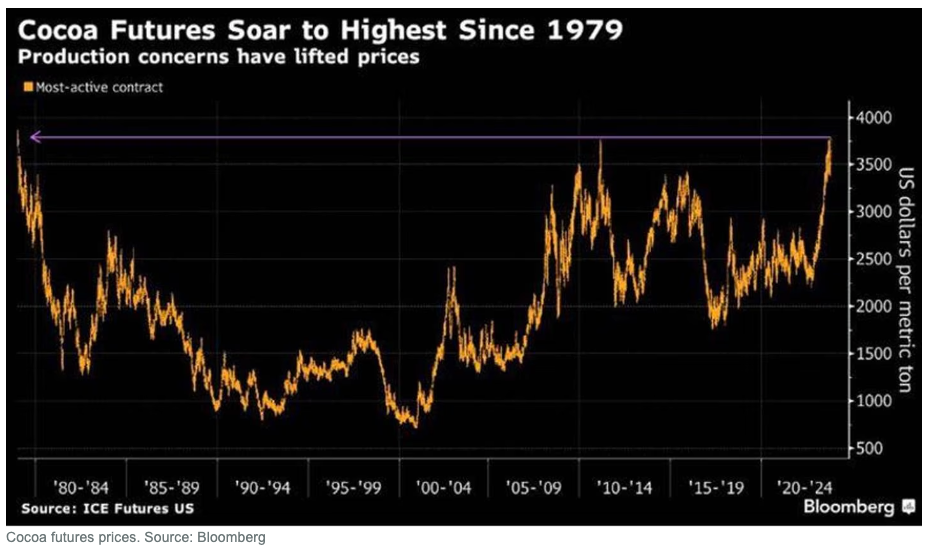

Just a few months ago in November 2023, we wrote a widely-circulated post detailing some of our observations at Uncommon Cacao around what were at that time the highest cocoa futures prices seen in nearly 50 years, at $4,000/MT. The futures market has not stopped climbing, peaking today at $6,884 for the March 2024 NY contract. Prices are up 45%+ YTD – as in, since January. And from what we’re seeing, they are likely to maintain the upward trend.

Why?

The biggest reason is supply

- Cote d’Ivoire is the largest cocoa producer in the world, and dynamics in this country heavily impact price. Today's government data showed Ivory Coast farmers shipped 1.16M MT of cocoa to ports from October 1 to February 25, which is down 32% from the same time last year. Last month, the Ivorian cocoa regulator halted forward sales of cocoa for the 2024/25 season until it had a better picture of production in the current crop.

- Ghana cut its production forecast for the current crop down to 650-700k MT, a 14 year low, indicating that unfavorable weather, disease (swollen shoot virus) and smuggling have contributed to the dramatic decline in production this year. Experts watching the country suggest production could end up as low as 570k MT this year.

- Other key producing countries such as Ecuador, Peru, and the Dominican Republic have faced significant supply shortages this year, primarily due to drought conditions caused by El Niño. Mexico’s harvest has been abysmal, leading grinders and traders from Mexico to seek cocoa throughout Central America, and in turn to Central American processors now seeking cocoa in the Caribbean and beyond.

- Supply is under pressure in many places around the world (although not all!), and as a result experts predict a cocoa deficit of up to 500k MT this year. This will be the third consecutive year of deficits, making this current era likely the largest shortfall of cocoa supply… ever.

Are farmers actually benefiting from these market dynamics?

- Not in Cote d’Ivoire and Ghana, the two countries most responsible for driving up the price. The farmgate prices in both countries were set before the market started rising at its current pace, which means Ghanaian farmers are receiving between $1,800 and $1,900 per ton of cocoa and Ivorian growers about $1,600/MT.

- Meanwhile, producers in neighboring countries such as Guinea, Liberia and Togo are earning as much as triple those prices or higher. While news is coming out of large smuggling shipments being stopped by authorities in both Cote d’Ivoire and Ghana, there is no doubt cocoa is flowing across the borders and this is impacting official numbers.

- Across Latin America, Southeast Asia, and other countries in Africa, many farmers are indeed benefitting from much higher farmgate prices than they have earned in the past. In Uganda, for example, where we reported a nearly $4,000/MT farmgate price back in November, farmgate price is now ~$5,650/MT and continuing to rise. In the many cases, this is fantastic, and cacao producers finally have an opportunity to earn more for their hard work!

- For some producers, including in Ecuador, Peru, and Guatemala, overall production is down, and the onslaught of climate-related issues (drought, disease, migration) alongside lack of investment in improved practices is causing frustration and limiting the actual impact of these prices for families.

- When bulk cocoa is priced higher than specialty, quality issues become a challenge. Producers may ask themselves: Why spend the time and effort complying with quality standards and practices if I can get such a high price from the buyer who requires nothing?

- The situation is challenging for many actors across the value chain, including aggregators and exporters whose cash needs have tripled in order to buy cacao at skyrocketing prices, and who are often scrambling to beat out local competition for limited supply to fulfill their contracted sales.

How is this impacting demand?

So far, it’s still a little too early to tell.

- That said, Hershey announced that sales fell more than 6% during Q4 as consumers didn’t purchase as much of their confectionery products as expected.

- On January 12, the National Confectioners Association reported that 4Q North American cocoa grindings fell -3.0% y/y. Similarly, the Cocoa Association of Asia reported that Asian Q4 cocoa grindings fell -8.5% y/y and the European Cocoa Association reported that European Q4 cocoa grindings fell -2.5% y/y.

- Retail chocolate prices are reportedly up 17% over two years and will keep rising.

- Overall, expectations are that chocolate consumption will go down as prices continue increasing. “Shrinkflation” and similar dynamics are likely. We can also expect to see more non-chocolate ingredients making their way into chocolate products, from palm and other vegetable oils to… lab-grown cacao?

What else is going on?

- Hedge funds are hungry to profit off the current volatility. This month the Financial Times reported that hedge funds are a record $8.7 billion deep in cocoa gambling. As former Cargill trader Martijn Bron states, “Hedge funds are not the cause of the rise, but in a lower liquidity market environment, they can amplify fundamentally justified market moves to extreme levels.”

- Most cocoa traders / buyers will hedge their purchases using futures contracts, helping to offset any impacts of price volatility. However, in order to play in the futures market, traders are required to maintain an equity account that covers a percentage of the underlying value of their futures contracts. When the market moves, futures brokers demand that traders deposit enough cash to meet their equity obligations, or their futures will be involuntarily liquidated. This can translate into huge sums of cash owed overnight on a regular basis as the market moves dramatically, as it is doing now. Margin calls, combined with significant delivery risk, could be pretty dangerous for players of all sizes in the trade.

Oh right, also, EUDR

At the Chocoa and World Cocoa Foundation events in Amsterdam earlier this month, it was clear for all that the EU Deforestation-free Regulation (EUDR) is absolutely happening – and yet there is no doubt that it will only intensify the supply scarcity for the European Union, which is by far the largest importer of cocoa and cocoa products globally. Even before the escalating supply challenges of the last few months, there was concern that there simply would not be enough proven deforestation-free cocoa to import into Europe by the compliance start date of December 31, 2024.

Some historical perspective

This concise deep dive into the history of cocoa production, prices, and geopolitical market dynamics gives fantastic insight and demonstrates that the modern market context is still quite young (and malleable) when compared to how long this plant has been part of human civilization.

Our take on it these days

It is unlikely the market will “recover” or “correct” to lower prices anytime soon. In fact, it seems more likely that ~$4,000/MT+ may become more or less the new baseline expectation for bulk cocoa prices for potentially the next decade, a ~50% increase over trading prices of recent decades. There is indeed a “perfect storm” of variables impacting cacao production, from not-so-temporary climate shocks, to systemic devastating disease, to aging & migrating producers, to limited planting of new trees, to new regulations limiting how land can be converted into new cacao farms, and so on.

As I argued in the last post, the externalities and true costs of modern cacao production which have been ignored for decades are coming home to roost. I think we may be looking at a hard reset for cocoa. Will sustained higher prices impact chocolate consumption? Certainly, at least in the short and medium term. Is it maybe not so much of a bad thing if the world eats less cheap confectionery chocolate? I would (controversially) say so, and it seems others would too.

Is it maybe better, in the long run, for some cacao producing families to convert to other, more profitable crops or income sources during this volatile period and to prevent dramatic income shocks to millions of families if/when the market eventually comes down? While this is a hard one to swallow, I do think the answer is ultimately yes. If current price levels can be maintained through stabilized fundamentals, we will be much closer to enabling a living income through cocoa farming as an industry.

We all know how the system works. We know that there will be a crash after the bull rally. We know how damaging this will be for producers.

So why not, in this moment, choose to architect together a new future for cocoa? The thorny topic of decommoditization (which is NOT decommodification) deserves a whole other post. But right now there are open minds to creative solutions at levels one would not expect. This is exciting.

Personally, I am intrigued by the concept of price discovery via identification and valuing of intrinsic (quality but also cadmium) and extrinsic (deforestation-free, for example) attributes of cocoa. This idea was developed for coffee by Kim Elena Ionescu and the team who developed SCA’s new Coffee Value Assessment tool. There is a lot we can learn and absorb from other industries if we are willing to accept that our pre-existing system has structural problems.

So what does this all mean for me?

There is no doubt that these will be extremely challenging times for many in the sector. But - craft chocolate, this is potentially your moment! While you must be prepared for increased cacao prices in 2024 (we are projecting a minimum $2-3/kg increase across most regions where we source, possibly more as the market continues upward) and beyond, your business models typically do not see the cost of cacao as a primary driver of unit economics. Conventional chocolate, on the other hand, typically has much lower labor and other variable costs in their unit economics, and thus will be much more impacted by cocoa prices. As their retail prices increase, craft chocolate could be more competitive on the shelf / on the internet. We encourage you to optimize for the reality of this year and beyond!

We have a lot more to say and had to cut ourselves off before getting into the country and regional specifics.

Please reach out to us for more details on dynamics in specific countries and/or for further discussion: hello@uncommoncacao.com

{kind=link}